Skip to content

Home

Research

Papers

Coding

Articles

Software

Trading

Contact Us

Menu

Home

Research

Papers

Coding

Articles

Software

Trading

Contact Us

Coding

Backtest a Profitable Trend-Following Strategy using Python

Backtest a Profitable Trend-Following Strategy

Designing a Profitable Intraday Strategy Using Python and Alpaca

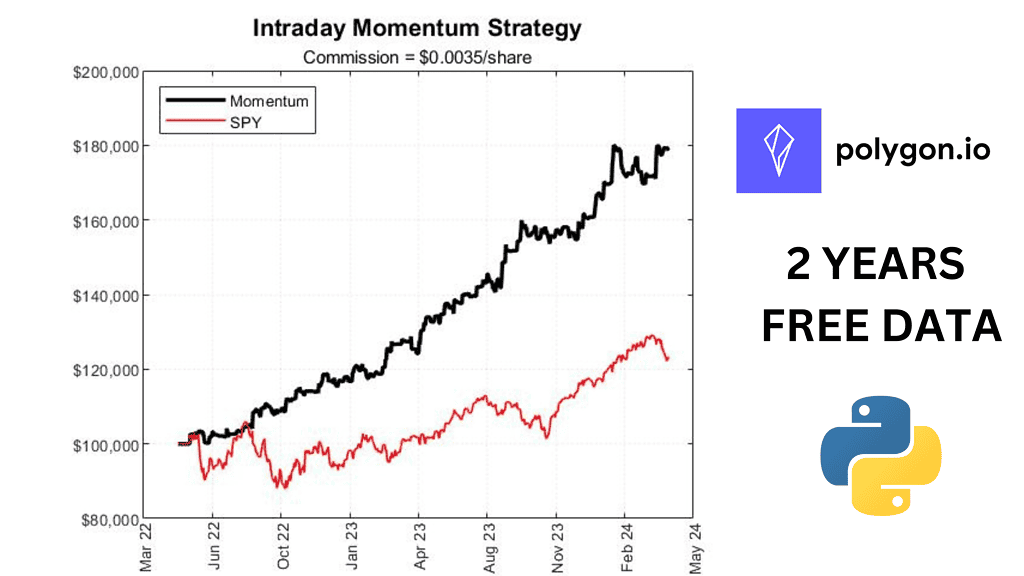

Backtesting 2 Years of FREE Data Using Python: Enhancing SPY Momentum Strategies with Polygon, from ‘Beat the Market’

MATLAB: Backtesting “Beat the Market: An Effective Intraday Momentum Strategy for the S&P500 ETF (SPY)”